If you currently invest or are thinking about it, one major thing you need to consider is how taxes reduce the value of your investments.

Taxes, just like fees, have a massive impact on your investment returns as they accumulate and compound over the long term.

In the UK, investment returns are seen as income and are therefore taxed.

The amount of tax you pay will depend on the amount you’re investing, your returns (profit) and the assets you’re investing in.

Source: MoneyWeek

Although UK citizens enjoy up to £12,300 tax free from profit generated after selling goods or investments, you will have to pay tax above this amount.

Types of Taxes in the UK

There are various types of taxes every investor in the UK needs to be aware of. These are;

1. Income Tax

Investment income comes in two ways; dividends and interest payments. This income is liable to tax and the amount paid depends on the tax band you fall into. Follow this link to learn more about income taxes in UK.

2. Capital Gains Tax

The goal of investing is that you sell your assets when they increase in value. Capital gains tax is the tax on the profit you make from this sales. If you buy shares at £300 and sell them for £700, you’ve made a capital gain of £400 which is subject to tax.

3. Stamp Duty Reserve Tax (SDRT)

This happens usually when buying shares online. You will pay a Stamp Duty Reserve Tax of 0.5%, taken automatically at the time of the purchase.

To find out more about taxes, visit this gov.uk page on personal tax.

How Can I Avoid Paying So Much Tax?

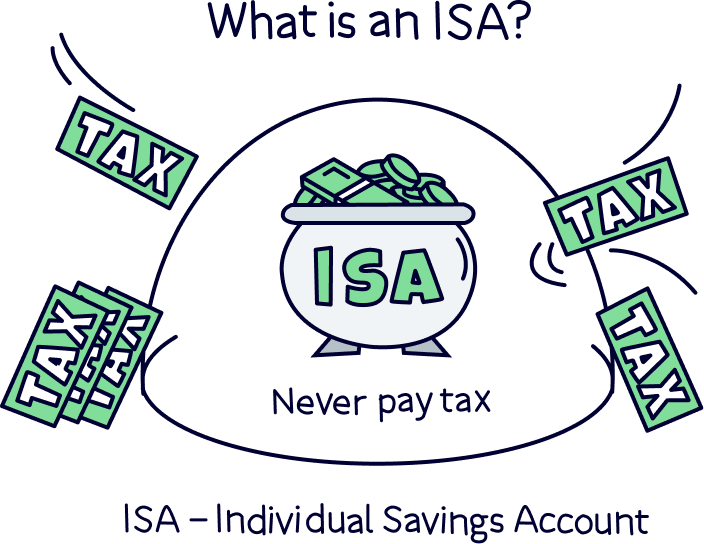

Introducing ISAs

ISAs are tax efficient ways of not just saving but investing your money. They are not liable to be taxed up to £20,000 each tax year (6th April one year to 5th April the following year). This means that you don’t pay any tax on the income from dividend payouts or capital gains from selling your investments at a profit.

How ISAs Work

Each tax year, your ISA allowance is reset and you get a new one. As said previously stated, each individual gets an allowance of £20,000. You can choose to split your allowance across the 4 different types of ISAs (which I will highlight below) or choose to have them all in one.

I like to split mine between the Stocks and Shares ISA and the Lifetime ISA.

ISA allowances cannot be carried over. If you do not use your entire allowance in the tax year, it will be lost.

Types of ISAs

There are about 4 different types of ISAs available for UK investors. When choosing yours, it’s advisable to consider which best suits your financial goals and risk profile.

You can have multiple ISAs but can only open one of each account in each tax year.

1. Stocks and Shares ISAs

This is the most popular type. They allow you invest in a diverse range of assets such as stocks, REITs, investment funds, trusts, bonds and more.

Image Source: Freetrade.com

To be eligible, you have to be;

- 18 or over

- Resident in the UK or a Crown servant working overseas

- Or married to/in a

civil partnership with a crown servant

working overseas

2. Cash ISAs

A Cash ISA is very similar to an everyday savings account except any interest it pays will be tax free.

With this, your money is usually invested in

- Savings in bank and building society accounts

- Some National Savings and Investments products

- Some life

insurance policies

To be eligible, you have to be;

- 16 or over

- Resident in the UK or a Crown servant working overseas

- Or married to/in a

civil partnership with a crown servant

working overseas

Tip: If you’re looking to save money in the short term, perhaps saving for a new car, or would like to build up an emergency fund, then check out Cash ISAs. The only downside is that their interest rates aren’t appealing.

Image Source: money.co.uk

3. Lifetime ISAs (LISA)

This is designed to help people save for their first home or for retirement. The great thing about this type of ISA is that the government will give you a 25% bonus of what you pay in each tax year. This means that for every £1 invested, the government will give you 25p.

You can only save/invest a maximum of £4,000 (not excluded from the total ISA allowance of per £20,000) tax year.

Using a LISA, you can invest in stocks, funds and cash.

To be eligible, you have to be;

- 18 or over but under 40

- Resident in the UK or a Crown servant working overseas

- Or married to/in a

civil partnership with a crown servant

working overseas

4. Innovative Finance ISA

They contain peer-to-peer loans instead of stocks and shares or cash. Peer-to-peer lending matches investors with borrowers.

Your money is usually invested in;

- Peer-to-peer loans

- ‘Crowdfunding debentures’ – investing in a business by buying its debt

- Cash

To be eligible, you have to be;

- 18 or over

- Resident in the UK or a Crown servant working overseas

- Or married to/in a

civil partnership with a crown servant

working overseas

You can either choose to have your entire £20,000 allowance split across the 4 different types of ISAs or have them in one.

I like to split mine across the Stocks and Shares ISA and LISA as they allow me to invest in the stock market and get the most returns for my money.

I also like to max out my LISA first as acts a huge advantage towards buying my first home.

Conclusion

Depending on your financial goal, ISAs are great tools to help make things easier and improve the value of your savings and investments.

Putting money away in an ISA is one of the best ways to prepare a solid foundation for your financial future.

But it doesn’t stop there!

To build wealth, you will have to use your ISAs to invest in the stock market.

In my investment workshops, I have broken down all you need to know to be a successful investor, visit my website now to book one of my workshops.